The statistics, charts, and graphs in this publication were updated as of June 8, 2026, to reflect the most current available data.

On January 23rd, 2026, the SEC continued its reset of long standing shareholder proposal and solicitation practices by revising Question 126.06 of its Compliance and Disclosure Interpretations (C&DI) on exempt solicitations. The Staff stated it would object to the voluntary submission of exempt solicitations from stockholders holding less than $5 million in company securities. The change follows a series of Commission actions that eased companies’ ability to exclude shareholder proposals and significantly reduced the SEC staff’s role in the no action process—developments that have altered how, and by whom, shareholder views reach the broader investor base.

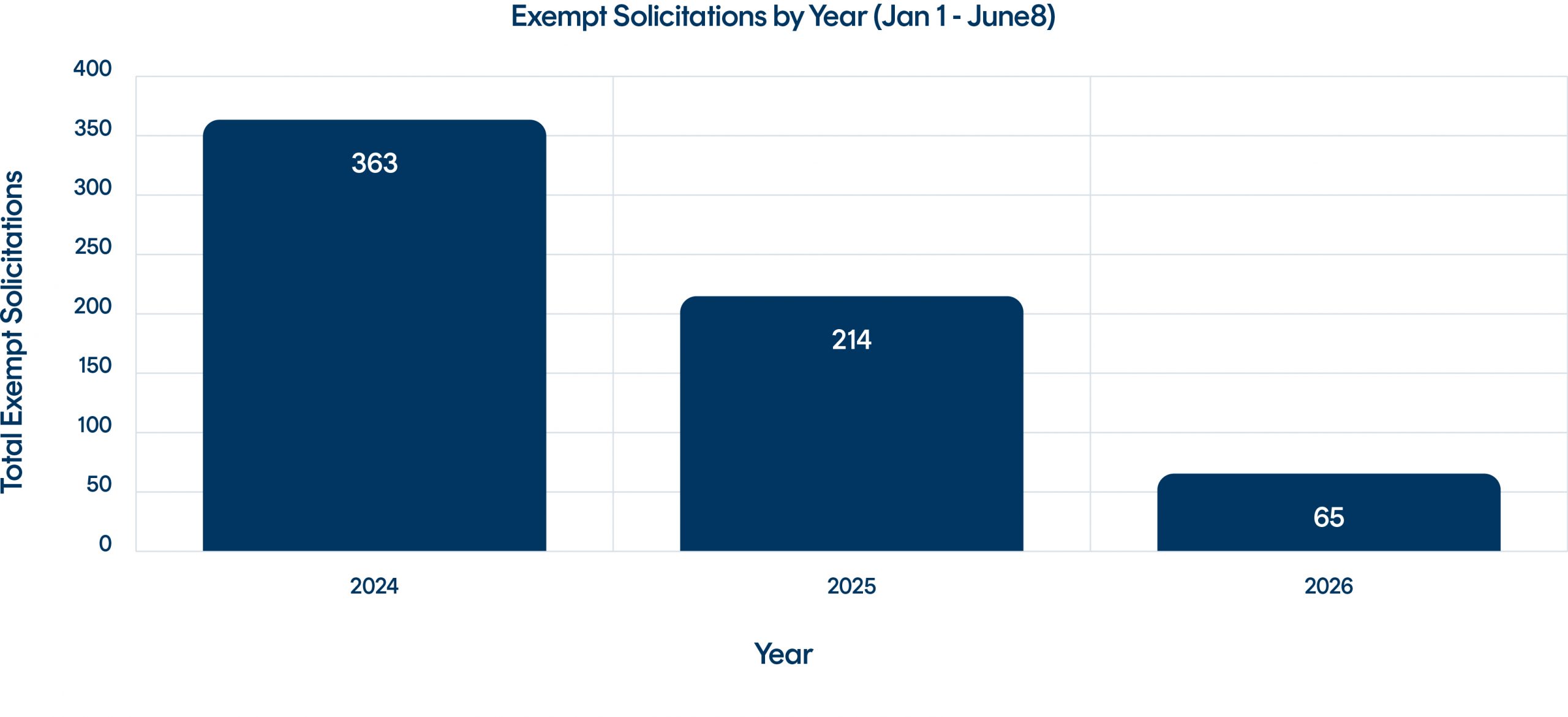

Since this revision went into effect, ISS has observed a significant decrease in the number of exempt solicitations filed with the SEC. Between January 1st and June 8th, sixty-five exempt solicitations were filed with the SEC. This is a notable decline compared to the same period in 2025 and 2024, in which there were two hundred fourteen and three hundred sixty-three exempt solicitations filed, respectively.

Vote No Campaigns

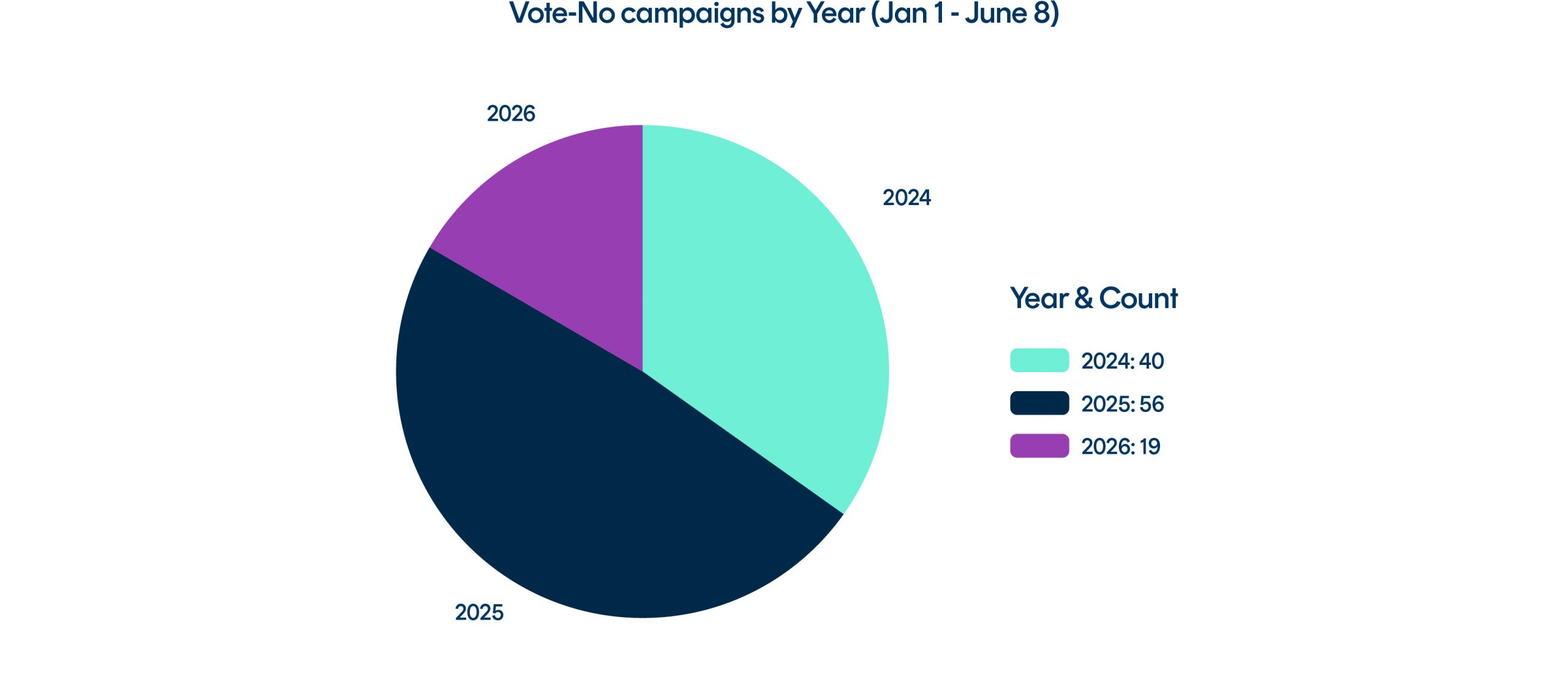

As of June 8th, 2026, nineteen filings have pertained to Vote No Campaigns (VNCs), six of which were in support of a VNC at Starbucks. This is a sharp decrease in VNC filings compared to 2025 and 2024, in which we saw fifty-six and forty filings, respectively, between January 1st and June 8th. It is important to note that all VNCs in 2026 were filed after the SEC’s policy change.

In previous years, VNCs were used to discourage support for a wide variety of proposals. In 2026, Fourteen of the nineteen VNC filings have been focused on director elections. For comparison, in 2025, seventeen filings pertained to non-election related management proposals (including eight filings for the same VNC at Amplify Energy Corporation) and sixteen filings pertained to shareholder proposals. In 2024, thirty VNC filings pertained to director elections, seven advocated against shareholder proposals, and three opposed a management proposal.

Filers

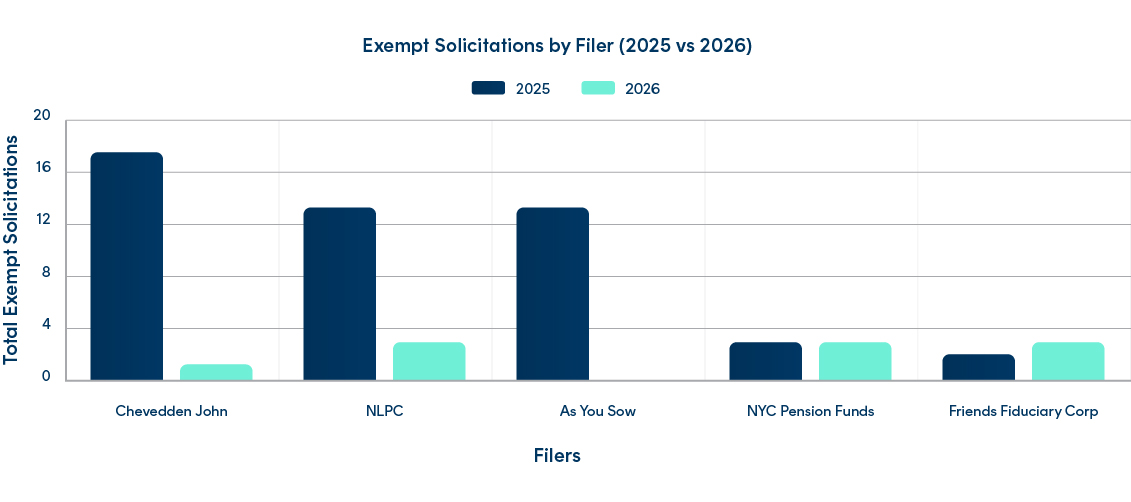

Shareholders who have historically submitted significant volumes of exempt solicitation materials through the SEC’s EDGAR filing system have been unable to do so this year. By June 8th of 2025, John Chevedden had filed twenty-two exempt solicitations, Bowyer Research had filed seventeen, the National Legal & Policy Center (NLPC) had filed sixteen, and As You Sow had filed thirteen exempt solicitations. In contrast, in 2026, NLPC has filed three exempt solicitations, John Chevedden filed one, and Bowyer Research and As You Sow have not filed any. It should be noted that the filings made by NLPC and John Chevedden were made before the SEC policy change went into effect.

Not all shareholders have been equally affected by the SEC policy change. The New York City Pension Fund filed three exempt solicitations during this period in 2025, and five filings in 2026. Additionally, Friends Fiduciary Corp filed five exempt solicitations in 2026, compared to only two filings during the same period in 2025.

Market Response

Some organizations are providing opportunities for shareholders to post their materials on privately owned, yet publicly available websites. These sites are examples of emerging market-based workarounds to the SEC’s crackdown on voluntary exempt solicitation filings.

The Interfaith Center on Corporate Responsibility (ICCR), for instance, has announced that it will post vote no campaign materials on its own website. The ICCR list includes the companies where proposals have been targeted by VNCs, the proponents, and a brief explanation of the reasons for the VNC.

Additionally, As You Sow has launched a site called Proxy Open Exchange, which provides a forum where shareholders can post their exempt solicitation filings. Many shareholders who have historically made use of exempt solicitations, including John Chevedden, Majority Action, Trillium Asset Management, and many others, have started using this site. The site lists the date of the filing, the filer, the associated company, and the proposal topic. Additionally, users can access pdf versions of the exempt filings.

While some have welcomed these initiatives as pragmatic efforts to fill the void, others argue that it does not constitute a comprehensive platform of record comparable to EDGAR. Materials posted on an organization’s website can be removed, edited, or replaced, and such sites are unlikely to capture the full universe of exempt solicitations across all proponents. Over time, however, these interim approaches may gain wider acceptance, or prompt the emergence of a more market driven solution that consolidates exempt solicitation materials from all parties in a single, durable venue. We will continue to monitor developments in this area as investors, issuers, and regulators adapt to the evolving mechanics of shareholder communication.

Conclusion

Early filings data from 2026 suggests that recent SEC policy changes have materially affected the volume and visibility of exempt solicitations, altering how shareholders express views on company performance and matters submitted for a vote. While a number of private, market-driven initiatives have emerged in response, it remains uncertain whether these alternatives will enable shareholders—particularly smaller proponents—to communicate with fellow investors and build support as effectively as they did under prior practices. The coming months should provide greater insight into whether these changes have material effects on shareholder participation, engagement dynamics, and voting outcomes at annual meetings.

Authored By

Mark Himes, Global Research, ISS Governance

See More