Key Takeaways

- The semiconductor industry primarily develops integrated circuits (i.e., chips) that are used in everyday products such as computers, phones, and cars. The industry faces vulnerabilities due to its unique supply chain interdependencies and geographical concentration.

- Semiconductor issuers are highly dependent on both specialized and manual labor for chip production. Lack of proper labor rights protections and inadequate worker conditions in the supply chain can lead to operational and market disruptions.

- When evaluated across three labor rights indicators, semiconductor issuers are setting robust labor standards but do not follow through on measures that protect suppliers from falling into non-compliance.

- Standard or Integrated Device Manufacturer companies (issuers who have in-house manufacturing) appear to have higher average scores on labor-related standards, procedures, and measures than fabless companies (issuers who outsource manufacturing). This difference in scores could indicate that when manufacturing is vertically integrated, as in a standard business model, it is easier to implement labor practices across the company’s value chain.

Semiconductors Are Necessary for Digital Life but Full of Social and Geopolitical Vulnerabilities

The world increasingly depends on semiconductors due to their prolific role in the production of everyday products, such as phones, computers, automobiles, and emerging technology and infrastructures, such as Artificial Intelligence and Data Centers.

At the same time, the industry also has a variety of vulnerabilities stemming from demand for both specialized and manual labor, global geopolitical interdependencies for raw materials and manufacturing, and supply-demand imbalances. These can be important considerations for institutional investors, as failure to prioritize labor rights and workers’ health and safety may lead to fines, operational disruption, and production shortages.

This article explores which labor risks are inherent in the industry and how to assess semiconductor issuers’ management of these risks in their supply chains. By exploring both the labor risks and risk management approaches, investors can have a better understanding of labor-related vulnerabilities latent in their portfolios.

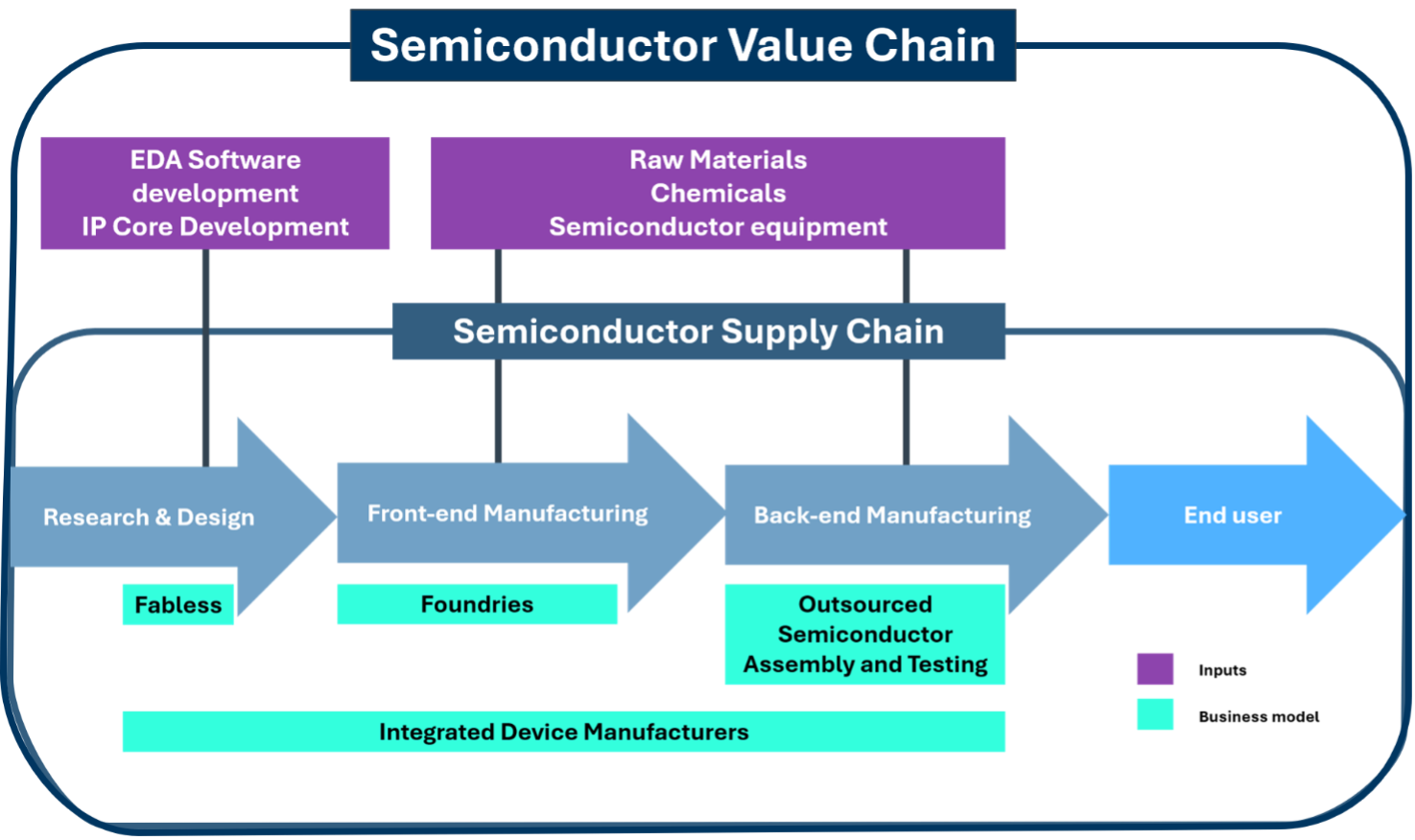

The Complex Circuit of the Semiconductor Value Chain

The semiconductor value chain is geographically concentrated with a range of inputs and outputs flowing across different parts of the globe to create integrated circuits (also referred to as “chips”). The indirect segment of the value chain includes the raw materials (i.e., critical minerals such as silicon) needed to make the chips, the software required to design chips, and the equipment that permits chip assembly into other products such as computers.

Due to the vast environmental and social vulnerabilities within the wider value chain, this article focuses on the direct semiconductor supply chain, from chip ideation to the end user of the chip (Figure 1), which includes other sectors such as Automobiles and Electronic Devices & Appliances.

Figure 1: Semiconductor Value Chain and Semiconductor Supply Chain

Source: ISS STOXX Research Institute, adapted from Global Supply Chains, Value Added and Production Intensity: Case Semiconductors.

Note: ISS STOXX refers to Integrated Device Manufacturers as Standard Semiconductor issuers

As shown in Figure 1, the semiconductor supply chain comprises three general parts: Research & Design; front-end manufacturing of the chip, also referred to as “wafer fabrication”; and finally back-end manufacturing, which includes the assembly and testing of the final product. South Korea and the United States are the main design contributors in the semiconductor market, while China, South Korea, and Taiwan play major roles in both the front and back end manufacturing components of the supply chain.

This geographical concentration developed because most companies in the industry usually specialize in one stage of semiconductor chip development (see Figure 2 below), For example, a fabless company focuses purely on design, while a foundry focuses only on front-end manufacturing.

Because all parts are necessary for the final product, the industry is increasingly dependent on strong supply relationships to develop necessary chips. Without this cooperation, the value chain could face multiple supply chain disruptions.

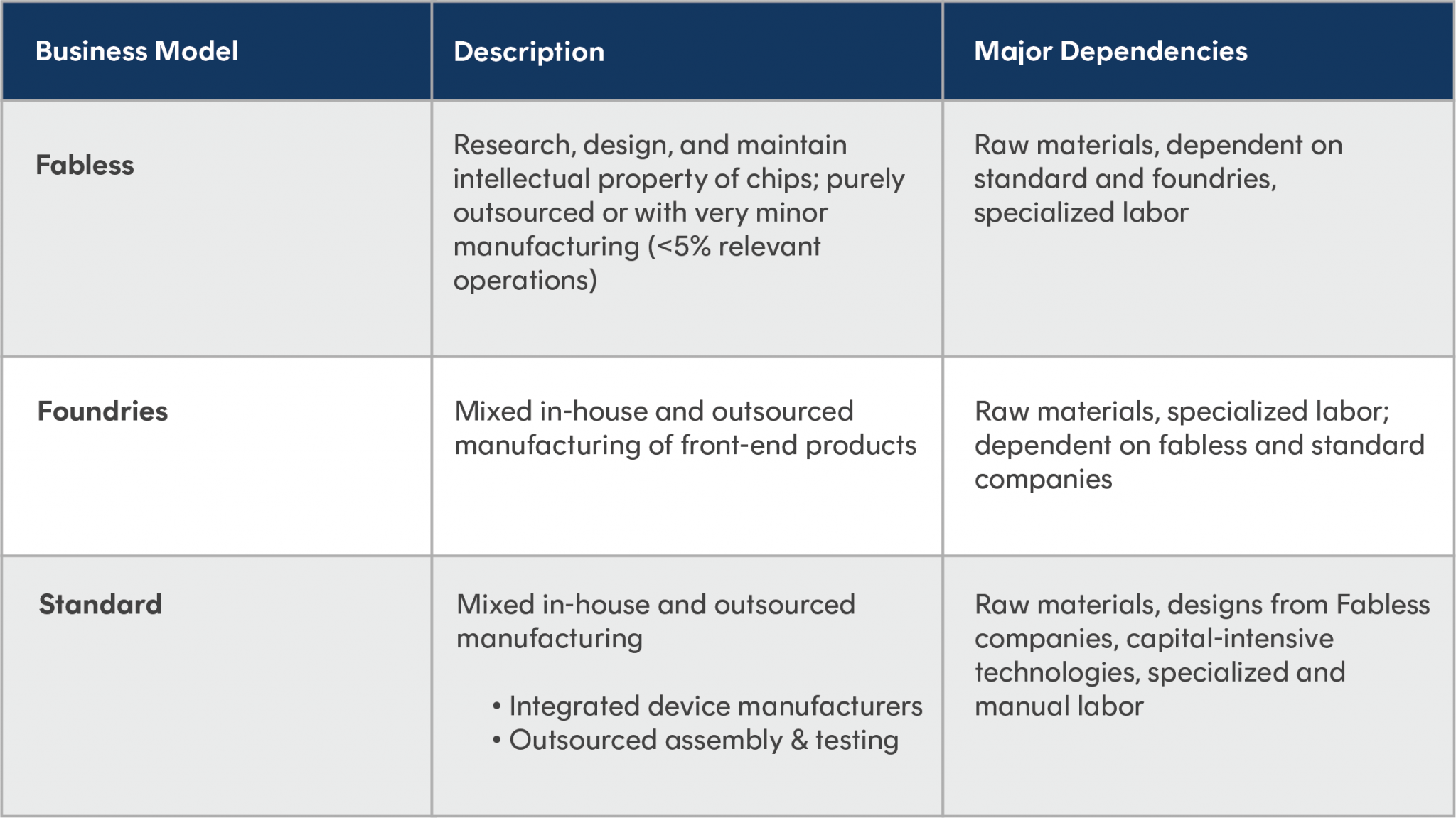

There are four primary business models that ISS STOXX considers when performing sustainability analyses on semiconductor issuers. The business models are Standard or Integrated Device Manufacturers (IDM), Fabless and Foundries (Figure 2).

Figure 2: Semiconductor Industry’s Main Business Models

Labor Risks in the Semiconductor Supply Chain

Human rights risks are diffused throughout the semiconductor industry, with more visible human rights violations demonstrated at the very beginning of the supply chain, through raw material extraction (for an expanded view into the human rights risks of the raw material supply chain, see the ISS STOXX series on sustainability considerations related to critical minerals) and manufacturing. As there are different business models in the semiconductor industry (Box 1), there are also different supply chain labor risks associated with each model, because some companies are more vertically integrated than others.

Vertical integration typically grants companies’ greater direct control over their manufacturing labor practices.

But both Standard (which mainly consist of Integrated Device Manufacturers) and Fabless business models often depend on low-cost, outsourced labor for back-end manufacturing, an approach to manufacturing that is also referred to as Outsourced Assembly, Testing, and Packaging. This labor is essential to the supply chain and often relies on migrant laborers. For example, in the United States around 43.9% of chip workers are foreign-born, usually coming from Vietnam and Mexico, and in Taiwan a large amount of chip workers come from the Philippines. According to the International Labour Organization, migrants are more than three times more likely to be coerced into forced labor practices than non-migrant workers due to need and economic challenges. Without proper due diligence, manufacturing workers can face illegal overtime hours, debt bondage, and increased probabilities of retaliation from self-advocacy, challenges which can devolve into forced labor.

Workers can also face occupational health and safety issues as they are surrounded by hazardous chemicals, indoor air pollution, and arduous repetitive movements.

Semiconductor Companies’ Unbalanced Relationship with Suppliers

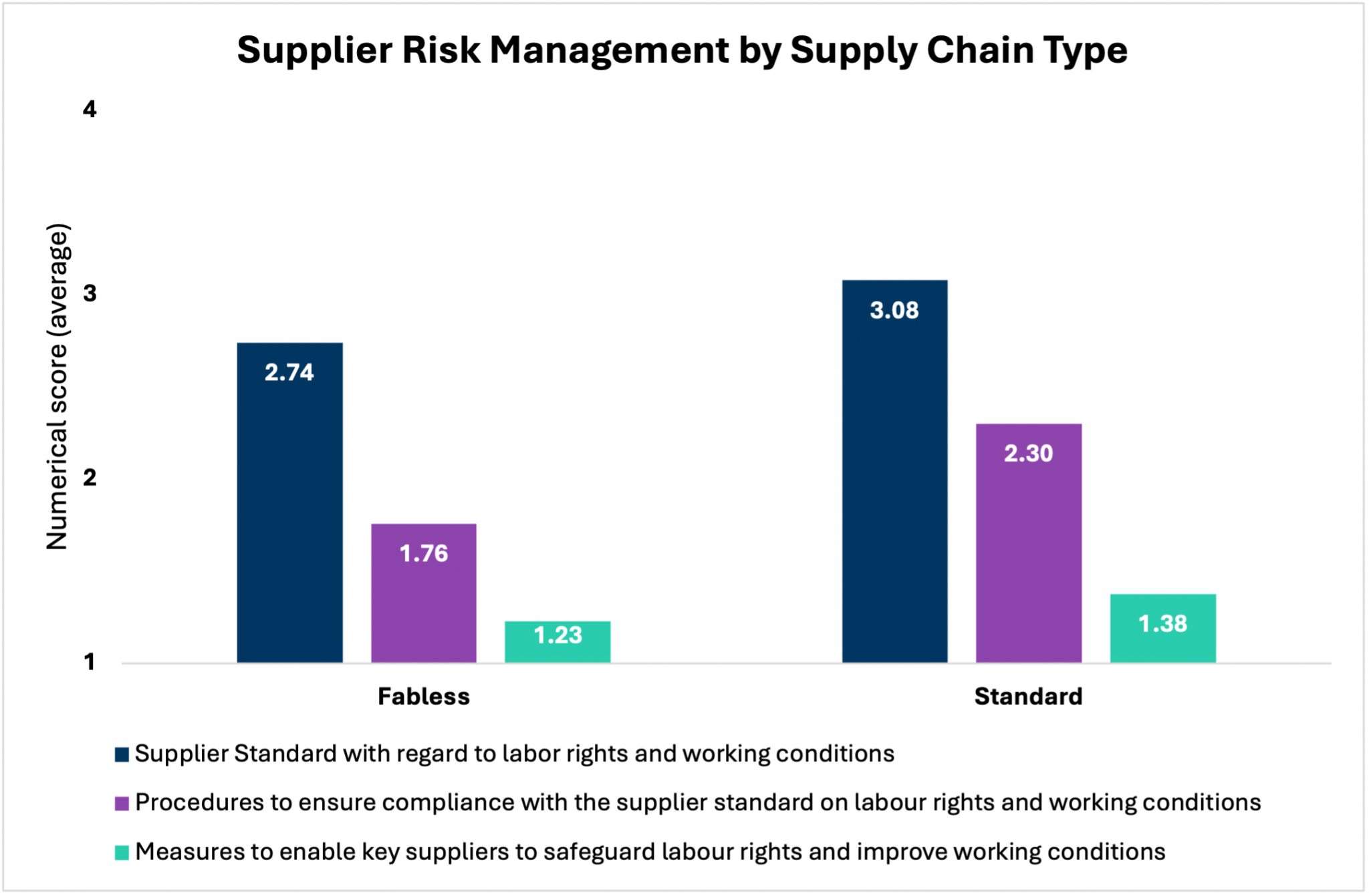

The ISS STOXX Research Institute analyzed the labor-related measures of 107 semiconductor companies, of which 43% were fabless issuers and 41% were standard issuers.

There are three primary indicators related to labor risk management in the supply chain, including:

- “Supplier Standard with regard to labor rights and working conditions,” which assesses the comprehensiveness of the standard in covering labor rights such as forced labor, child labor, and wages.

- “Procedures to ensure compliance,” which evaluates whether procedures, including risk assessments and audits, are properly in place to ensure adequate compliance with the supplier standard set.

- “Measures to enable key suppliers to safeguard labor rights and improve working conditions,” which assesses whether a company has protocols, such as fair and responsible purchasing agreements, in place to protect workers in its supply chain from abuse.

Figure 3: Supplier Risk Management by Semiconductor Business Model

Source: Corporate Ratings, data as of May 2026

Within the supply chain, risk management is unbalanced. Figure 3 demonstrates that, on average, supplier standards are robust but issuers fall short in ensuring their internal procedures and measures, such as adequate contract timing, create the conditions that permit their suppliers to stay in compliance with the standards set.

To re-iterate, having a supplier standard is worthwhile, but it is only the first step toward wider risk mitigation. Without strong procedures and measures to follow, human rights and labor rights risk mitigation could leave issuers both at risk of fines and supply chain disruptions.

Standard companies appear to have higher average scores on labor-related standards, procedures, and measures than fabless companies. This difference in scores could indicate that when manufacturing is vertically integrated, as in a standard business model, it is easier to implement labor practices across the value chain.

Conclusion: Labor is a Key Dependency for the Semiconductor Industry’s Continued Success

The semiconductor industry is a critical player that enables connectivity, globalization, and technological advancement. At the same time, given the interdependencies across the semiconductor value chain, these companies are also highly dependent on specialized and manual labor, making labor rights an important consideration for investors. Exposure to labor rights risks can lead to fines, operational disruption, and production shortages.

Our research demonstrates that issuers categorized under the standard business models, issuers who mainly have in-house manufacturing, appear to have better scores for standards, procedures, and measures in place to ensure supplier labor rights and working conditions in comparison to fabless issuers, who outsource most of their manufacturing.

Your Feedback Matters

Let us know how this research resonated with you. Your input helps us develop content that resonates with investors across the globe.

Authored By

Caitlin Harris, Research Lead, ISS STOXX Research Institute

Andres Del Gallego, SEMI Specialist, Corporate Ratings, ISS STOXX

Gayathri Hari, SEMI Specialist, Corporate Ratings, ISS STOXX

Emily Helms, Corporate Ratings Researcher, Corporate Ratings, ISS STOXX

See More