Key Takeaways

- Financed emissions are the greenhouse gas (GHG) emissions attributed to a financial institution’s lending and investment activities.

- Disclosure momentum is accelerating: reporting of financed emissions has been growing at an average annual rate of 70% since 2021, driven by the adoption of reporting standards.

- Quality assurance has become a prerequisite for meaningful peer benchmarking, engagement prioritization, and trend analysis.

- Regional divergence is noted, as European banks lead on disclosure while Asia and other regions remain at earlier stages of adoption.

- Data quality gaps remain material, with only one‑third of reporting banks fully aligned with PCAF guidance on Scope 1, 2, and 3 disclosures, limiting comparability across peers.

- Enterprise Value Including Cash (EVIC)-based peer group comparisons reveal hidden risk, showing that banks with similar balance sheet scales can exhibit vastly different financed emissions profiles due to lending strategy, sector exposure, portfolio coverage, and assets type.

Introduction

Understanding financed emissions is increasingly central to managing climate risk and identifying opportunities in the transition to a low‑carbon economy. Capital allocation decisions shape real world emissions: this influence has prompted investors to look more closely at how financial flows either accelerate or hinder the transition to a low-carbon economy.

While banks have made meaningful progress in measuring their operational emissions, emissions linked to financing activities (that is, emissions generated by funded companies and projects) remain more challenging to assess. These emissions are reported under Scope 3, Category 15 (Investments) and are particularly material for financial institutions. Frameworks such as the GHG Protocol and the Partnership for Carbon Accounting Financials (PCAF) have brought greater structure and consistency to this once‑opaque area, referring to such emissions as “financed emissions.”

In recent years, financed‑emissions reporting has accelerated globally, providing investors with a clearer view of how banks’ balance sheets intersect with climate outcomes and financial materiality. This reporting trend is consistent with IFRS S2 requirements.

Yet the real analytical challenge for investors is no longer whether financed emissions should be disclosed but how those disclosures should be interpreted. As reporting expands, headline financed-emissions values alone reveal little unless accompanied by clarity on portfolio boundaries, asset-class coverage, and inclusion of investee Scope 3 emissions. In this sense, the emerging differentiation among banks lies not only in the level of financed emissions reported, but in the quality, completeness, and decision-usefulness of the disclosure itself.

This article examines the evolution of financed‑emissions disclosure, its growing relevance for investment decision-making, and the limitations of current disclosures.

Financed Emissions Standard Development

The Greenhouse Gas Protocol (GHG Protocol) released the Scope 3 Standard in 2011, providing guidance for calculating emissions across 15 categories of Scope 3 activities that encompass both upstream and downstream operations. In 2015, the Partnership for Carbon Accounting Financials (PCAF) was established by 14 financial institutions with the objective of developing a standardized methodology for measuring and disclosing greenhouse gas emissions associated with financial activities. The initiative gained broader acceptance in subsequent years, with 50 financial institutions joining by 2019. That same year, PCAF launched a global standard for measuring Scope 3 Category 15 (financed emissions) activities across six asset classes. This standard was subsequently reviewed by the GHG Protocol in 2020. The standard was further updated in the year 2022 and most recently in the year 2025, expanding its coverage to 10 asset classes.

Trend of Scope 3 Financed Emissions Reported Data

The Insights article More Disclosures, Less Clarity: The Scope 3 Data Quality Challenge discussed broader Scope 3 emissions reporting trends. Within the financial sector specifically, reporting of Scope 3 Category 15 (financed emissions) has historically been limited.

The banking sector companies in the ISS STOXX Climate Database number around 1,400, which represents a 6% increase since 2021. However, Category 15 reporting has grown more rapidly during this time.

Financed emissions reporting in the Climate Database increased by an average of 70% annually between 2021 and 2024. The proportion of database banks disclosing financed emissions correspondingly rose from 5% to 21% within three years. This trend is largely attributable to the growing adoption of standardized and consistent reporting frameworks for financed emissions.

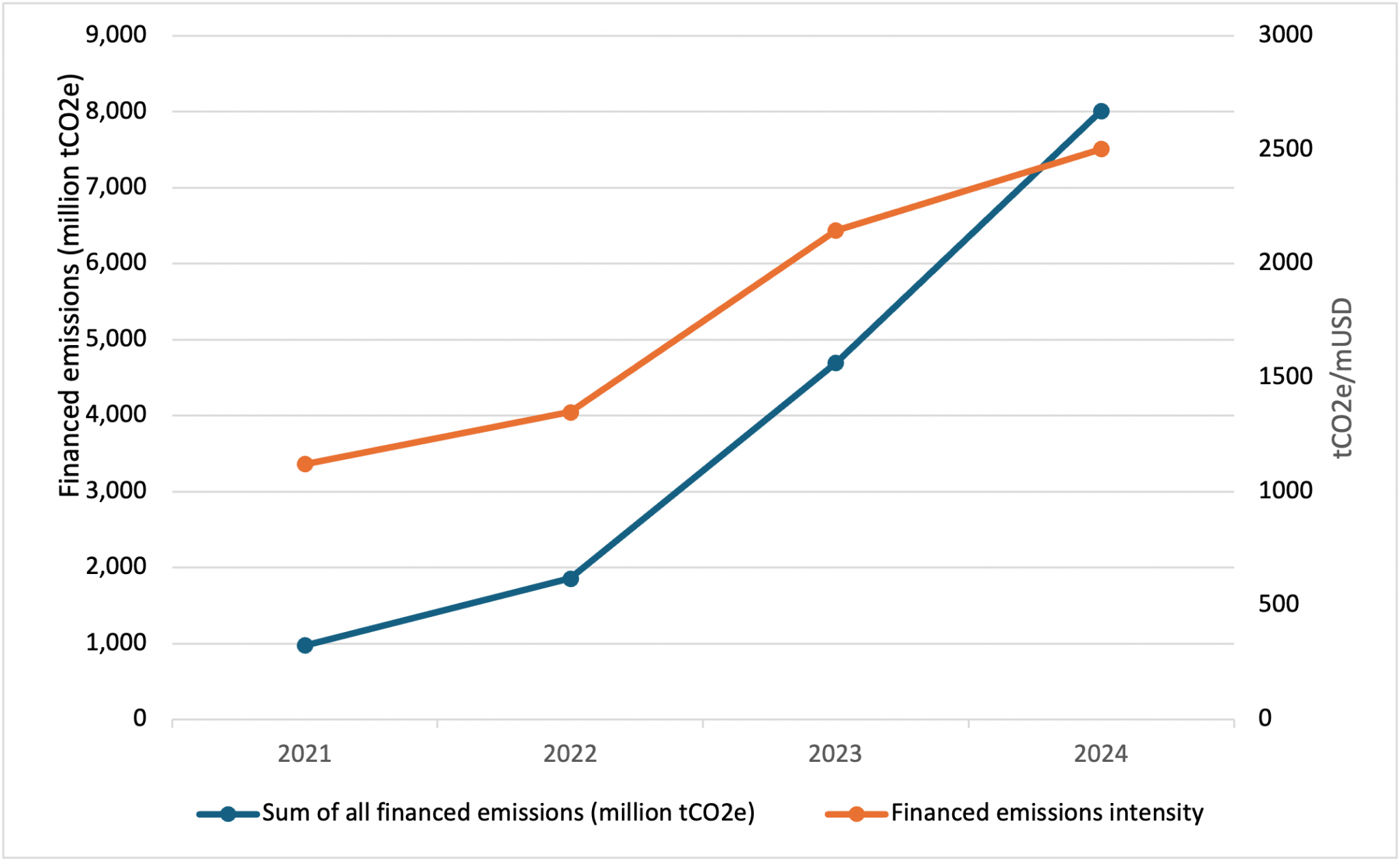

In absolute terms, total financed emissions of banks in the Climate Database increased from 976 million tCO₂e in 2021 to 8,015 million tCO₂e in 2024, representing an increase of 721% over four years. Financed emissions intensity with revenue follows a similar trend, where we can see a steady rise in the past three years (Figure 1).

Figure 1: Historical Trend of Scope 3 Financed Emissions and Intensity with Revenue

It is important to note that this sharp rise primarily reflects expanded disclosure coverage and methodological alignment. That is, the rise reflects a market moving from partial visibility toward fuller accounting of financed activities, rather than an equivalent increase in underlying real economy emissions.

Scope 3 Financed Emissions Reported Data Quality

As outlined in the article More Disclosures, Less Clarity on the quality review of Scope 3 reporting, the review process applied to reported data is both rigorous and highly stringent. Each company is subject to in‑depth quality review and can be excluded due to any of the following reasons: a) inconsistent boundary setting, b) a lag in the reporting of financed emissions, c) incomplete portfolio coverage, and d) vague reporting of financed emissions that may not account for all emissions-intensive financing activities.

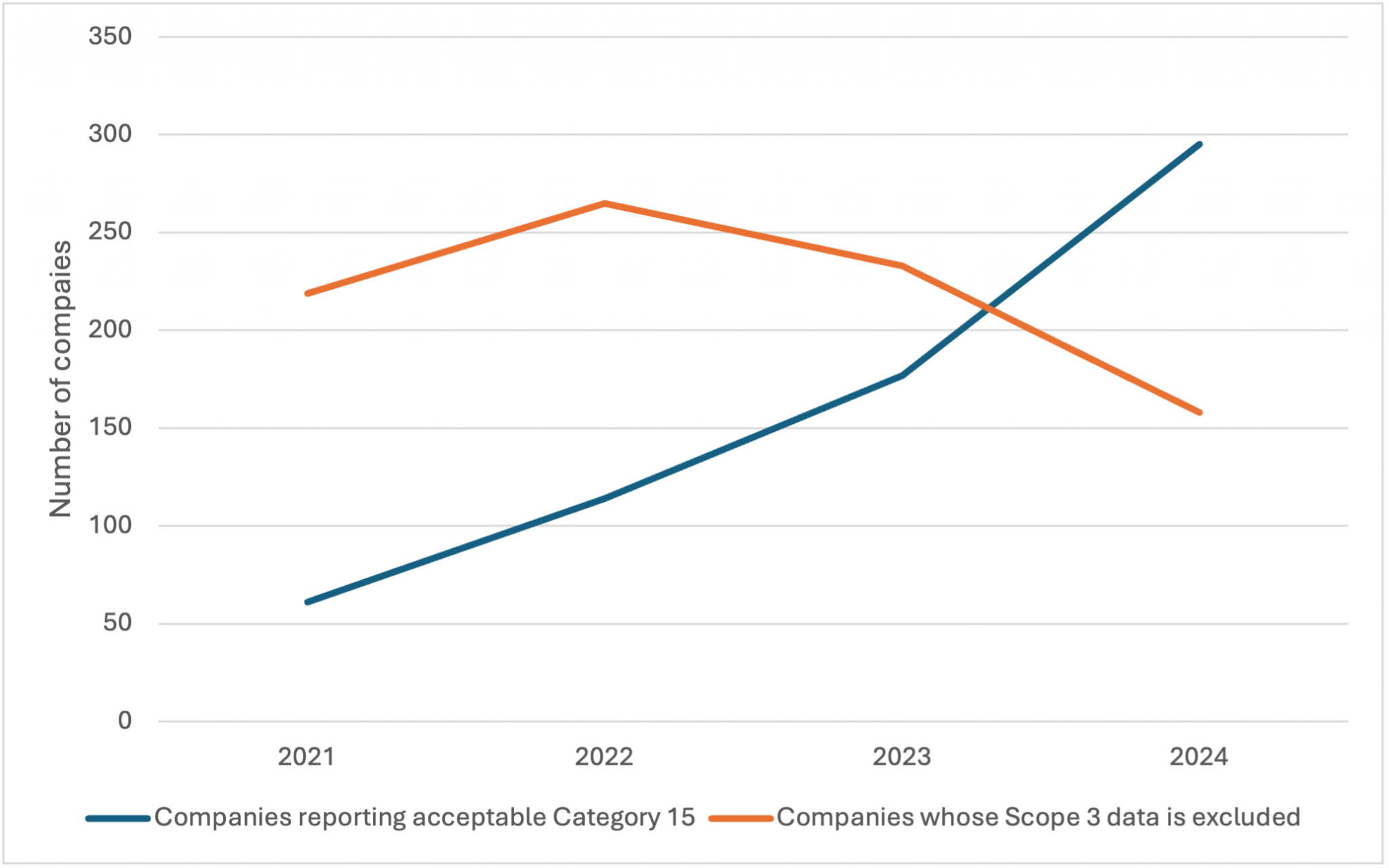

For FY2024, reported Scope 3 emissions data from more than 150 companies within the Banking sector were rejected following quality review and updated with modelled Scope 3 emissions data. Approximately 300 companies disclosed data that met the required quality parameters.

As illustrated in Figure 2, a clear downward trend in Scope 3 data rejection is observed alongside a steady increase in the number of Banking sector companies reporting Scope 3 Category 15 data with acceptable quality.

Figure 2: Trends in Banking Sector Companies’ Reporting of Scope 3 Financed Emissions

This pattern is expected to persist in the coming years, driven by factors such as the introduction of reporting mandates in certain regions and the growing adoption by countries of internationally recognized reporting standards. In regions where climate reporting requirements have matured, the trend is likely to hit a plateau. It will be interesting to see the direction of the trend, where there’s little or no clarity in terms of reporting mandates.

The distinction between reported and quality reviewed data has analytical consequences. For data users, poor quality financed emissions disclosure can be more problematic than non-disclosure because it may create a false impression of comparability across peers. Banks reporting partial portfolios, unclear boundaries, or incomplete inclusion of financed asset classes may appear to perform better or worse than peers for reasons that are methodological rather than economic. As a result, quality assurance becomes a prerequisite for meaningful peer benchmarking, engagement prioritization, and trend analysis.

Financed Emissions Disclosure Trends across Regions

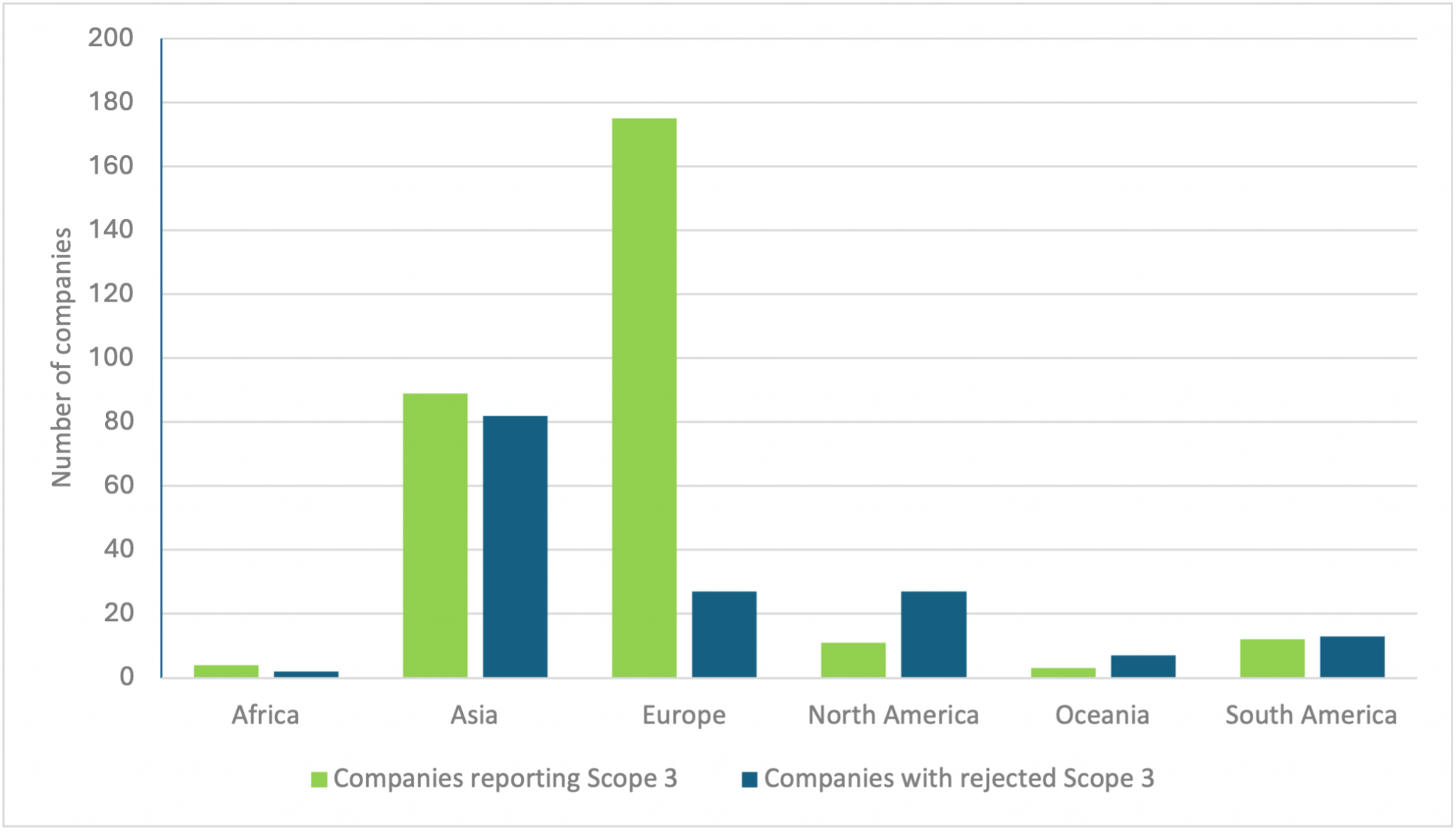

Among the financed emissions reported by Banking sector companies across the Climate Database, Europe leads in the disclosure of financed emissions in 2024, while other regions continue to refine and evolve their emissions reporting practices (Figure 3).

Figure 3: Disclosure of Banking Sector Companies, by Region, FY2024

Source: Climate Database

This leadership reflects the early and widespread implementation of regulatory frameworks and mandatory reporting requirements across European markets.

In contrast, regions such as Asia and Oceania remain in the adoption phase of internationally standardized reporting frameworks. Although reporting quality and coverage in these regions are improving, there remains significant scope for more consistent and sustained progress. The highest number of Scope 3 data rejections continue to originate from banks based in Asia, highlighting persistent challenges related to data quality and alignment with reporting requirements.

While this picture holds true for most countries in Asia, Japan seems to be taking long strides in financed emissions reporting. From our analysis of FY2024 data, Japanese banks’ reported financed emissions show better portfolio coverage, data quality with high PCAF scores, and overall greater clarity and granularity of underlying data.

How PCAF Changes Are Driving Scope 3: Financed Emissions

In the second edition of the Financed Emissions Standard, the Partnership for Carbon Accounting Financials (PCAF) specifies that financial institutions should include Scope 1, Scope 2, and Scope 3 emissions of investee companies when reporting financed emissions, with Scope 3 emissions disclosed separately. PCAF introduced the reporting of investee Scope 3 emissions through a phased‑in approach (Table 1).

Table 1: List of Sectors with Required Inclusion of Scope 3 Emissions

| Phase‑in period | NACE Level 2 (L2) sectors considered |

| For reports published in 2021 onwards | At least energy (oil & gas) and mining (i.e., NACE L2: 05–09, 19, 20) |

| For reports published in 2023 onwards | At least transportation, construction, buildings, materials, and industrial activities (i.e., NACE L2: 10–18, 21–33, 41–43, 49–53, 81) |

| For reports published in 2025 onwards | Every sector |

Source: PCAF Standard

Under this approach, investee companies in the energy and mining sectors were required to report Scope 3 emissions starting in 2021. From 2023 onwards, Scope 3 reporting requirements were extended to companies in the transportation, construction, buildings, materials, and industrial sectors. Ultimately, Scope 3 emissions across all sectors are expected to be included in financed emissions reporting by financial institutions.

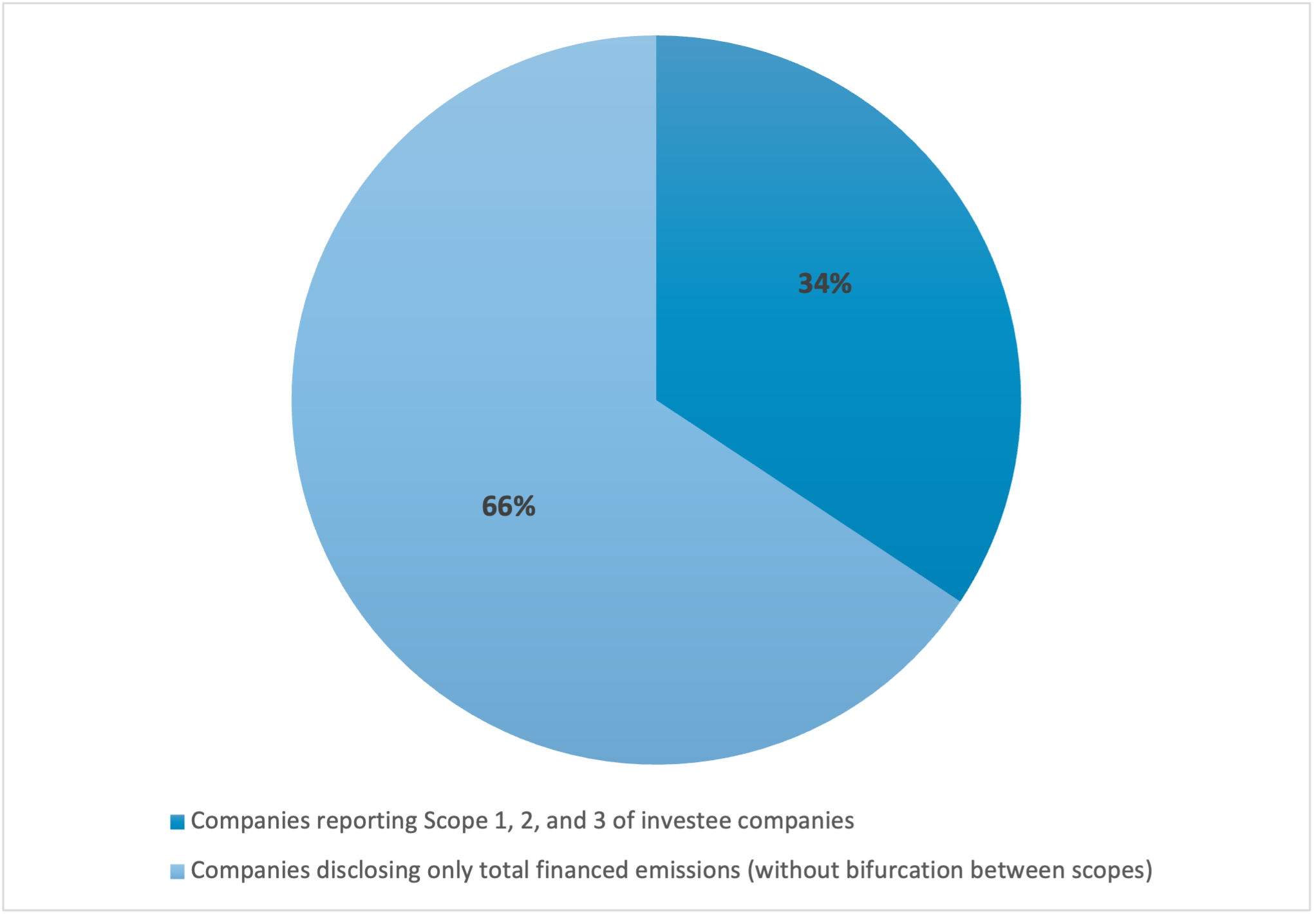

In FY2024, out of around 300 Banking sector companies reporting financed emissions within the Climate Database, only 34% adhered to PCAF guidelines by disclosing investee companies’ Scope 1, Scope 2, and Scope 3 emissions with appropriate clarity. The rest have provided limited clarity while disclosing Scope 1, 2, and 3 emissions of the investee companies or provided no details at all.

Figure 4: Share of Banking Sector Companies Disclosing Investees’ Scope 1, 2, and 3 Emissions, FY2024

Source: Climate Database

Financed Emissions Reporting with EVIC Lenses

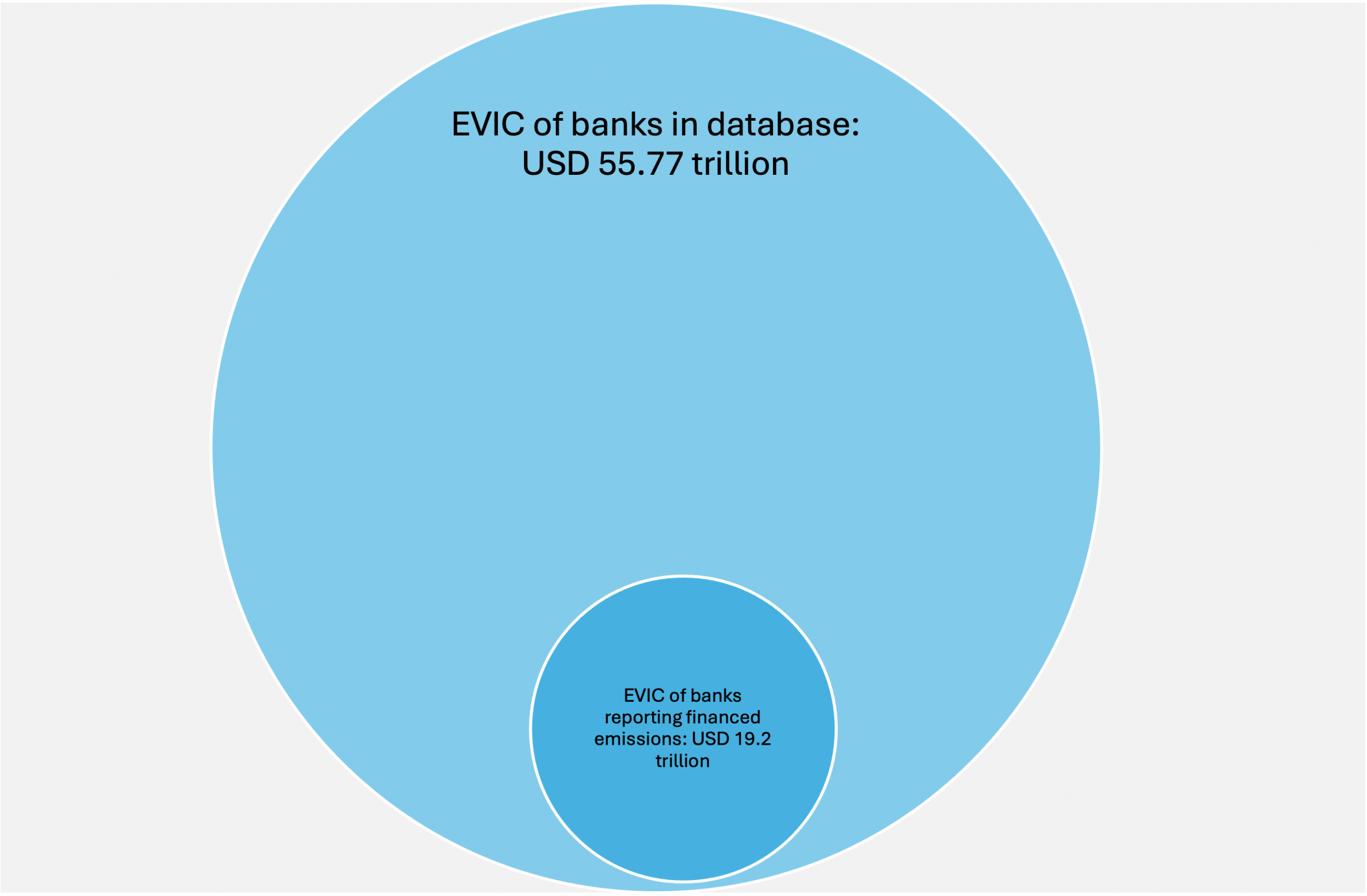

As of Q1 2026, the total Enterprise Value Including Cash (EVIC) of Banking sector companies covered in the Climate Database stands at approximately USD55 trillion. Companies that report financed emissions account for approximately USD19 trillion of this total, representing approximately 34% of aggregate EVIC. The remaining 66% of companies rely on ISS STOXX estimated financed emissions data to address disclosure gaps (Figure 6).

Figure 5: Share of Financed-Emissions Reporting Banks, by EVIC, Q1 2026

Source: Climate Database

While estimated data provides a reasonable high‑level view of banks’ financed emissions, it cannot fully capture the complexity of firm‑specific financing and investment activities, due to limitations in the availability of granular disclosures. These limitations become evident when comparing banking sector companies with similar EVIC profiles operating within the same geographic region, as illustrated in Figure 6.

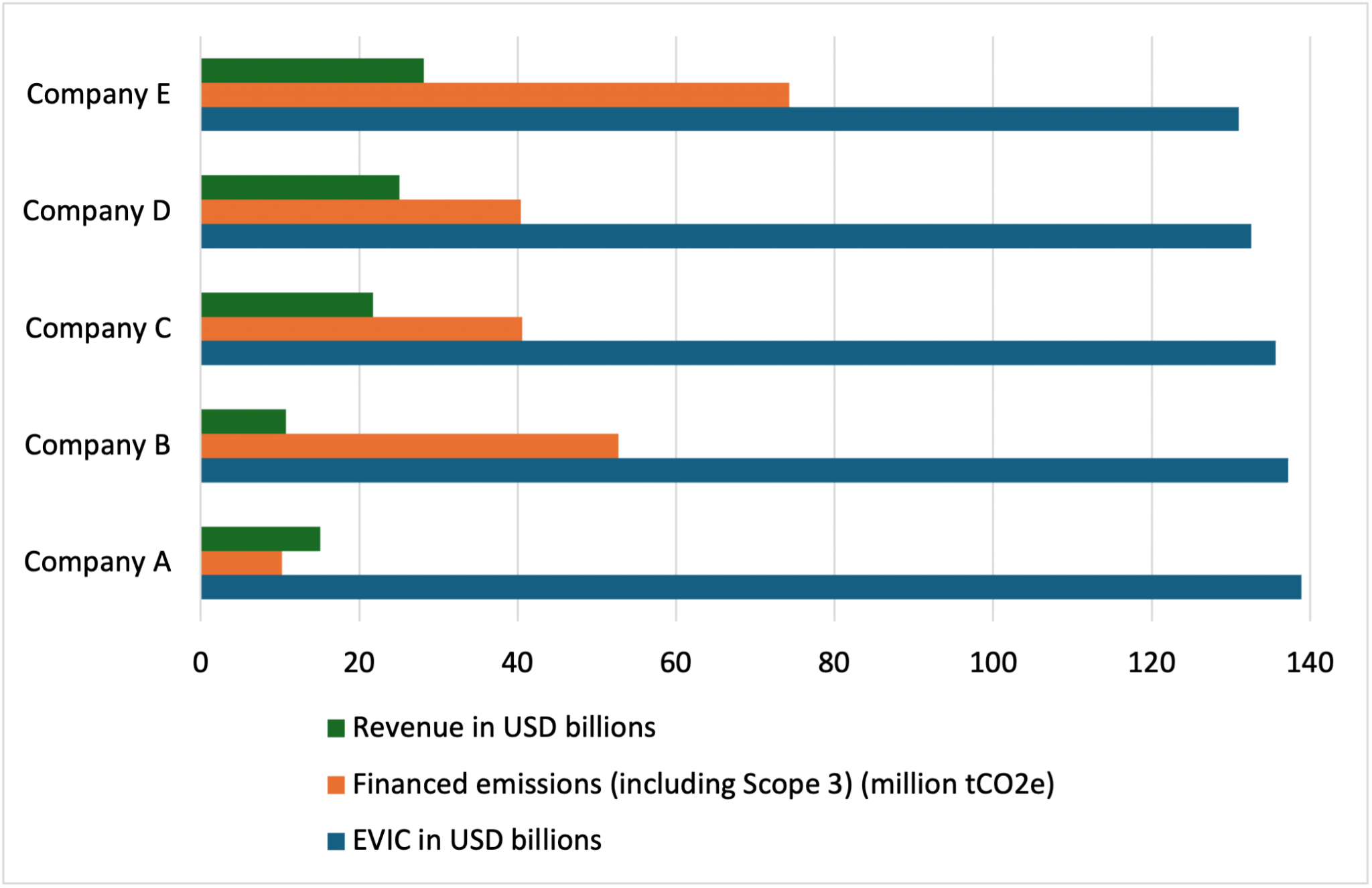

Figure 6: Comparison of Scope 3 Financed Emissions Data in Relation to EVIC, FY2024

Figure 6 compares banking sector companies with EVIC values within a similar range and shows substantial variation in their reported financed emissions (including Scope 3). For instance, Company A and Company E have EVICs of USD 138 billion and USD 131 billion, respectively, yet their reported financed emissions amount to 10 million tCO₂e and 74 million tCO₂e, respectively. Despite both companies disclosing investee Scope 1, Scope 2, and Scope 3 emissions as part of their financed emissions reporting, the magnitude of reported emissions differs markedly.

Such divergence may be attributed to several factors, including (1) differences in lending or investment strategies, where one company may have greater exposure to emissions-intensive sectors while another may be actively reducing such exposure; (2) variation in the coverage of financed emissions disclosures; and (3) differences in the asset classes included within financed emissions disclosures.

Conclusion

Financed emissions reporting has entered a phase of rapid expansion, offering investors an increasingly clear yet still incomplete view of how financial institutions influence real world emissions through capital deployment. While disclosure volumes and methodological sophistication have advanced meaningfully since 2021, material gaps remain in data quality, scope coverage, and cross-regional consistency.

Financed emissions are no longer a peripheral disclosure but a critical lens through which transition risk, capital alignment, and long‑term value creation must be assessed. Continued regulatory harmonization, improved Scope 3 data availability, and deeper alignment with reporting standards (IFRS S2 disclosure requirements) will be essential to translating disclosure momentum into actionable investment insight.

Your Feedback Matters

Let us know how this research resonated with you. Your input helps us develop content that resonates with investors across the globe.

Authored By

Samidha Shinde, Analyst, Climate Research and Analytics, ISS STOXX

Suman Karar, Analyst, Climate Research and Analytics, ISS STOXX

See More